- Jimmy Jean

Vice-President, Chief Economist and Strategist

Weekly Commentary

It May Be Time to Make Federal Spending Reviews Permanent

April 12, 2024

When the Canadian federal government released its 2023 budget over a year ago, it pledged to conduct a strategic spending review to find $15.4 billion in savings, including $1.3 billion from Crown corporations. The savings were supposed to offset the $43 billion in announced new government spending. It was an attempt to maintain fiscal credibility. The government had previously set a number of fiscal anchors, like keeping the deficit below 1% of GDP starting in 2027. But nearly a year after its announcement, the spending review has found just $9 billion in savings. Meanwhile the government has been announcing new spending measures every day for weeks now.

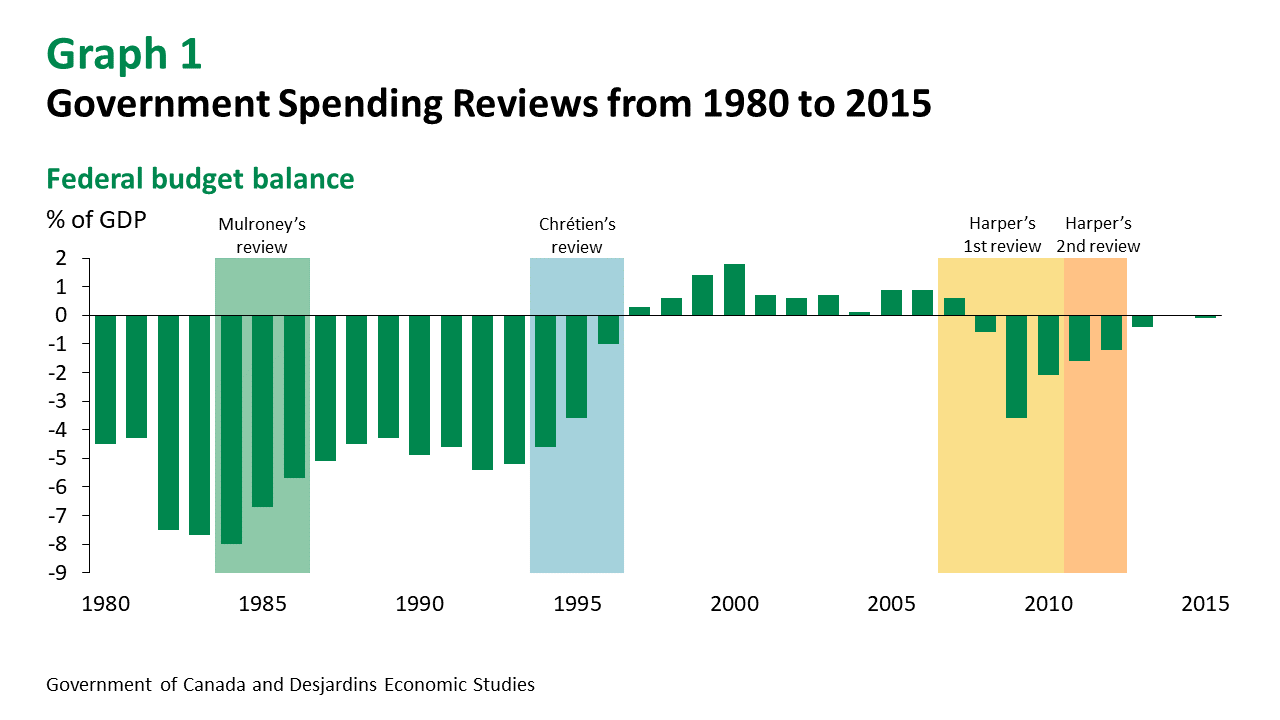

So what exactly is a spending review? It’s when the federal government takes a close look at its operations to either find savings and reduce the deficit, prioritize other spending or optimize the delivery of public services. Five such reviews have been conducted over the past thirty years by both Conservative and Liberal governments. The results have been mixed. The Nielsen review under the Mulroney government was poorly executed and failed to materially turn public finances around. Hence why, after taking office, Jean Chrétien’s Liberal government had to do its own review in 1994, with the deficit-to-GDP ratio approaching 5% (graph 1). Unlike his predecessor’s review, Chrétien’s led to real belt-tightening and laid the groundwork for the budget surpluses his government came to be known for.

Stephen Harper’s Conservative government inherited pristine public finances when it took over in 2006. To keep Canada’s fiscal house in order after cutting personal and corporate taxes, however, Harper faced some tough choices. But no sooner had he announced a spending review than the financial crisis hit. When the government conducted a second review in 2011, its stated goal was to return to a balanced budget—something it more or less did in the 2014–2015 fiscal year.

According to a report External link. by the C.D. Howe Institute, the success or failure of a spending review often hinges on political will. And that tends to be in greater supply at the beginning of a government’s mandate. But zealously pursuing unpopular measures can be politically treacherous. After conducting a provincial spending review, Premier Philippe Couillard implemented strict budget controls in Quebec, helping it lose the infamous title of Canada’s most indebted province. The Couillard government was subsequently routed at the ballot box in 2018.

The federal Liberals have learned you can’t run on fiscal restraint and win. (Some would say they’ve known it all along.) As a result, the 2023 spending review—announced alongside new spending—failed the sniff test. After all, our policymakers aren’t exactly known for budgetary discipline.

This begs the question: is it time to make spending reviews permanent? Countries like the Netherlands and Denmark conduct systematic, transparent, non-partisan reviews of their government spending, and their healthy public finances consistently earn them AAA ratings. So there is a blueprint for sound fiscal management that’s independent of the election cycle and occasional qualms about fiscal sustainability.

Canada’s debt looks pretty good compared to its international peers, but huge challenges lie ahead, including the climate transition, housing affordability and the aging population. The federal government will need to be as lean as possible. But to meet these challenges, trimming $15 billion here and there won’t cut it.

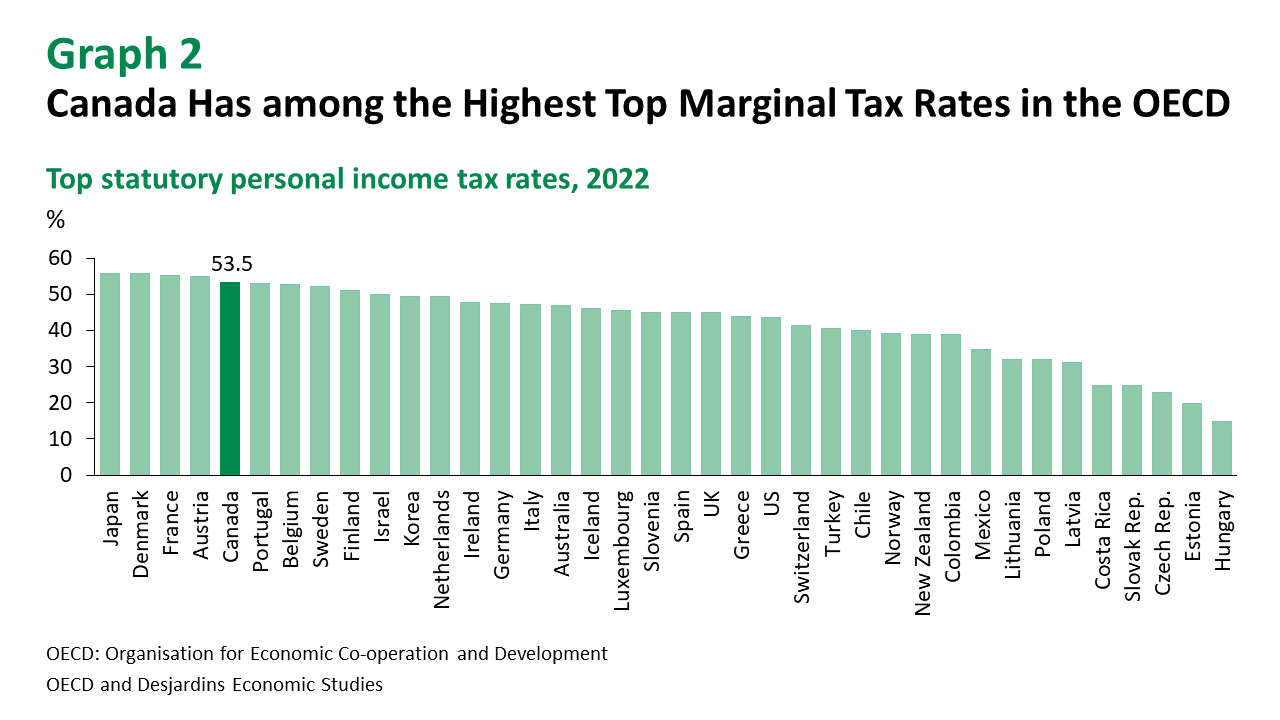

Once again, we as a nation need to ask ourselves some tough questions. First, given the challenges we face, what’s a realistic and sustainable debt level? Second, what tolerance do we have for approaching this limit, assuming we’re not already there? To answer this question, we also need to decide how to fairly distribute the financial burden of those major challenges between generations. Third, assuming we can’t get around these imperatives, how much can we leverage taxes given that Canada already has the fifth highest marginal tax rate in the world (graph 2) and needs to stimulate investment, not scare it away?

We as a country need to have a frank, forward-looking discussion about these issues. Labelling all new spending as bad—even necessary spending and real investment in the future—won’t get us anywhere. And any constructive debate must incorporate a counterfactual basis of comparison. At the same time, on the policymakers’ side, engaging in the occasional opaque, essentially symbolic spending review isn’t a real solution.

It will be difficult to meet all the challenges we face if we don’t increase government revenues. Don’t be surprised if Tuesday’s budget contains tax increases. (See our budget preview External link. for more.) But there is a tendency to underestimate how hard it is to raise taxes. Especially since capital, companies and brainpower know no borders and the 15% global minimum tax on multinationals is really just symbolic.

We’ve said it before and we’ll say it again: generating economic wealth by encouraging private investment External link. and boosting productivity is still the solution that checks the most boxes. The government needs to set a good example and—most importantly—send the right message. Canada’s political class has yet to put forward a concrete, cohesive plan to generate the wealth the country needs and keep public finances on a solid footing. And that’s a problem.