- Randall Bartlett

Senior Director of Canadian Economics

Essentials of Monetary Policy

The Bank Sets Up to Start Knocking Rates Down

April 10, 2024

According to the BoC

- As was widely expected, the Bank of Canada held the overnight policy rate at 5.00% today, where it’s remained since the July 2023 rate decision.

- Most importantly, the Bank opened the door to its next move being a cut, seemingly in the not−too−distant future. According to Governor Tiff Macklem’s Press Conference Opening Statement, “What do we need to see to be convinced it’s time to cut? The short answer is we are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained. The further decline we’ve seen in core inflation is very recent. We need to be assured this is not just a temporary dip.”

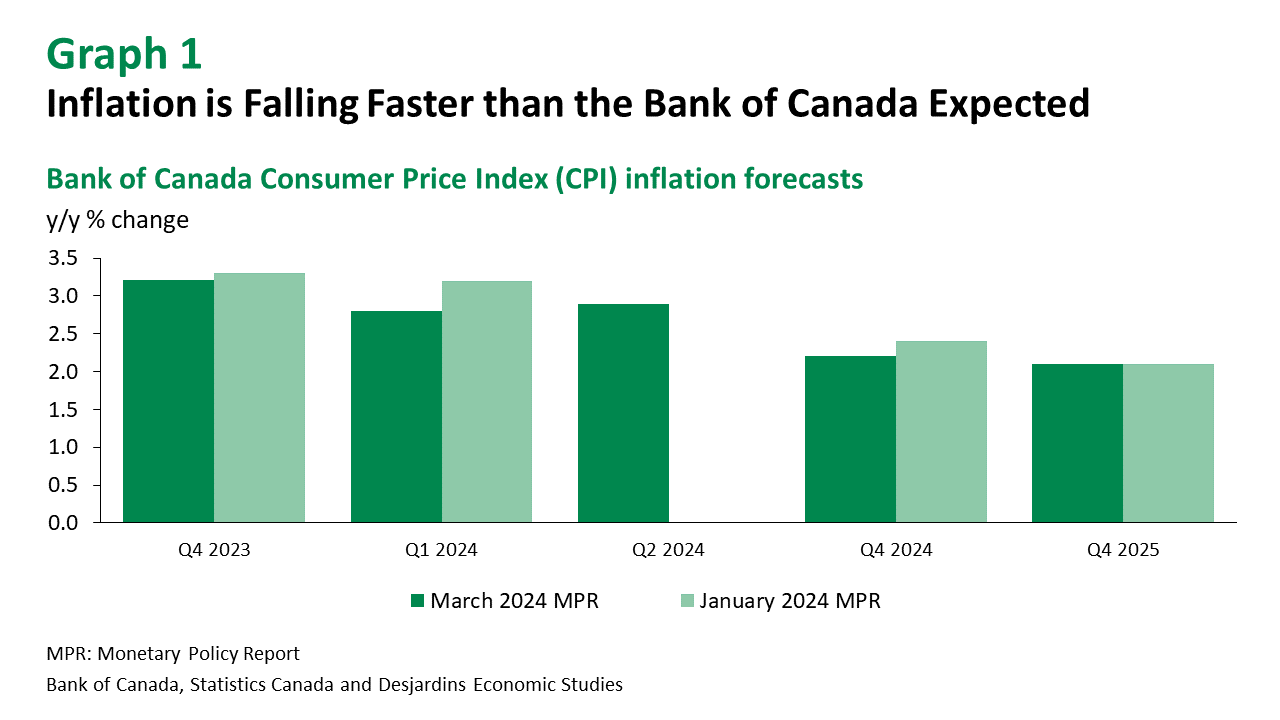

- In support of this more dovish turn, the Bank revised down its outlook for CPI inflation. This had to happen in the near term, as the inflation has come in below 3% y/y in the first two months of 2024, averaging 2.8% versus the Bank’s prior forecast of 3.2% for Q1 (graph 1). The Bank now expects inflation to average 2.6% for all of 2024 versus 2.8% in the January 2024 Monetary Policy Report (MPR), ending the year at 2.2%. In 2025, the inflation projection was left unchanged at 2.2%.

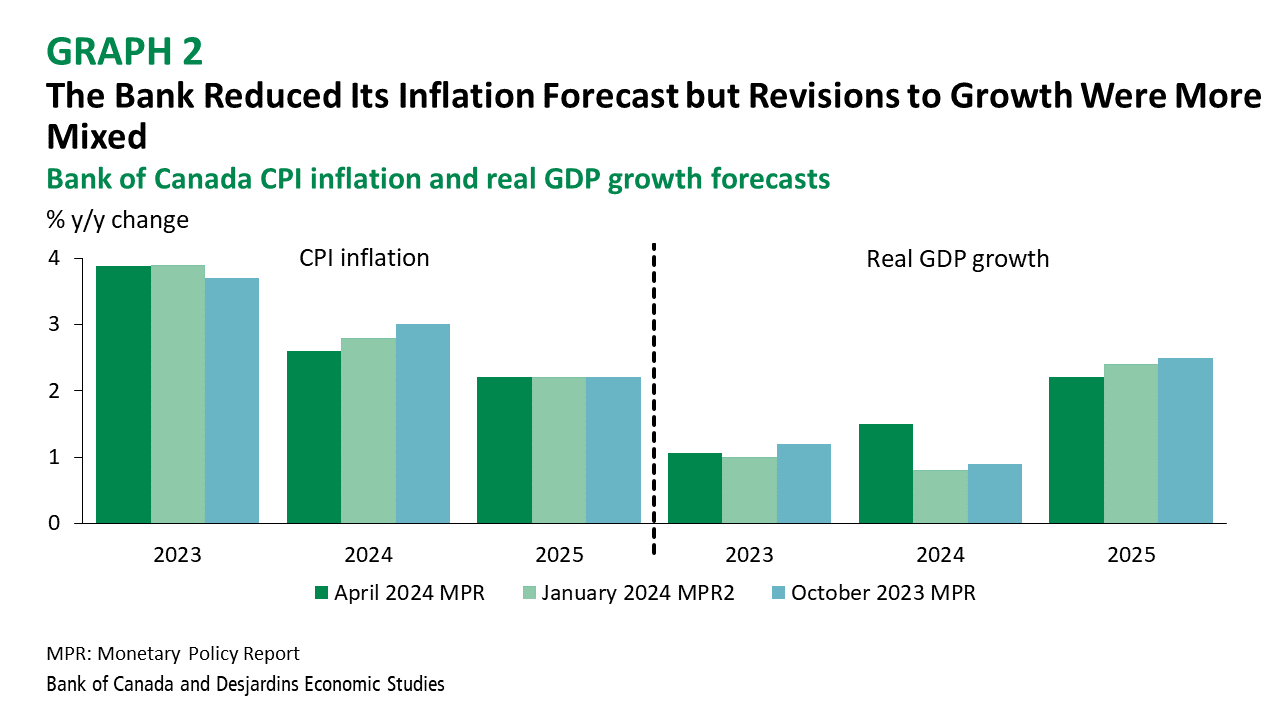

- Complementing the softer inflation outlook were mixed revisions to the real GDP growth forecast (graph 2). In the near term, it was inevitable that the Bank was going to have to revise up growth, as the data have been coming in too hot to ignore. Not only did the second half of 2023 come in better than expected, but the Q1 2024 tracking is much higher than previously projected (2.8% annualized versus 0.5%). As a result, the 2024 real GDP growth outlook was revised up from 0.8% to 1.5%. However, further out in the forecast, things are not quite so rosy. In 2025, growth was revised down to 2.2% from 2.4% in the January 2024 MPR. Part of this reflects the federal government’s recently announced plans to cap the share of non-permanent residents in the population. Our analysis suggests this could weigh heavily on real GDP growth going forward, albeit less so on inflation.

- It should be noted that the Bank also adjusted its estimate of the neutral rate of interest—the appropriate policy rate when inflation is at target and real GDP is at its trend level—slightly higher in today’s announcement, from 2.5% to 2.75%. With the policy rate unchanged, that suggests monetary policy may not be quite as restrictive as was earlier believed.

Implications

While keeping rates steady, as expected, the Bank’s openness to lower rates left little doubt what’s coming. The only question is when. The Governor observed that policymakers will track various inflation indicators “in the months ahead,” but suggested that their confidence in the disinflation process has continued to increase. As a result, we remain of the view that rate cuts will begin at the upcoming June meeting. Rates should move steadily lower thereafter as inflation gradually cools, while ongoing mortgage renewals and a slower pace of population growth weigh on economic activity.

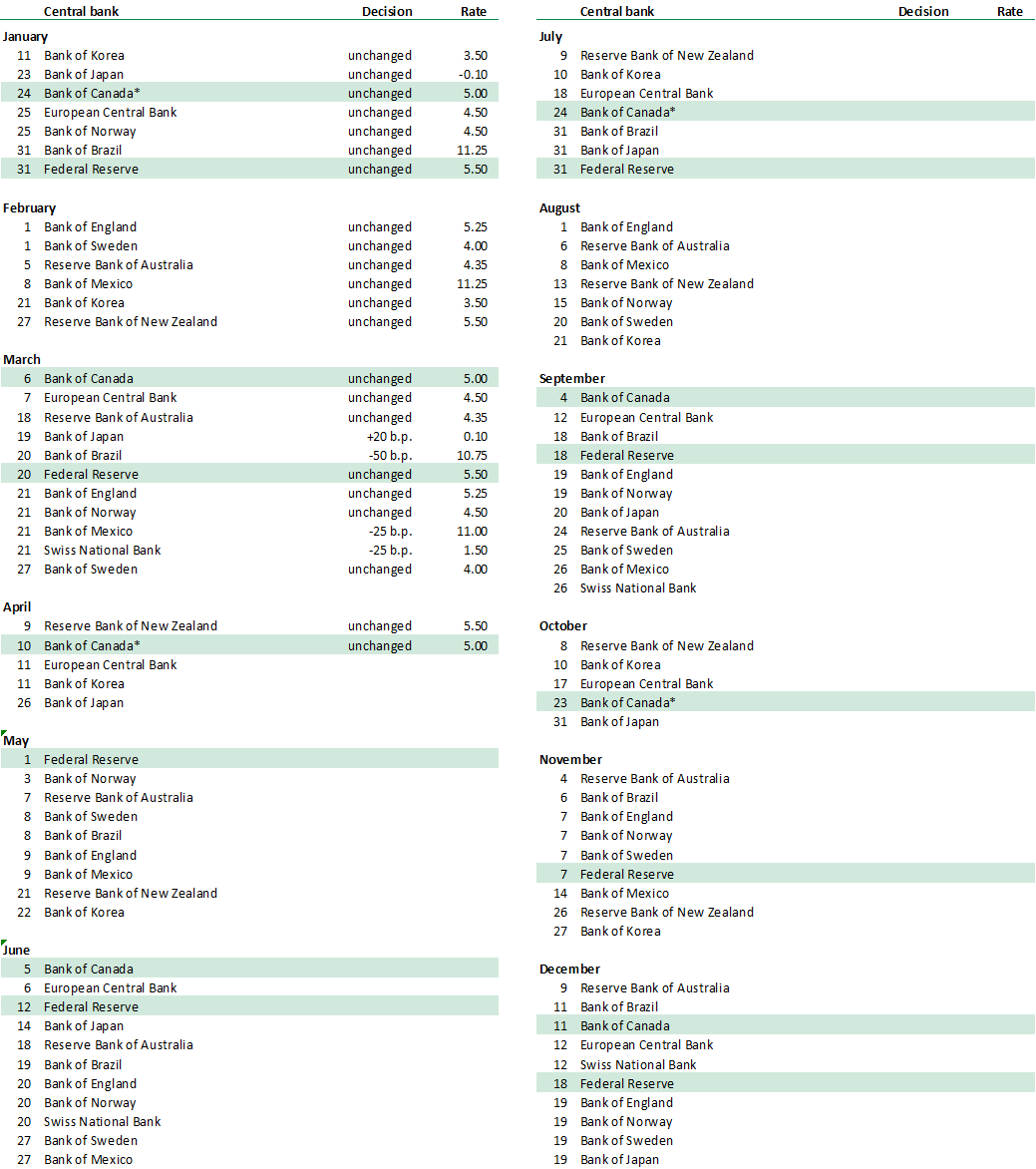

2024 Schedule of Central Bank Meetings