-

Florence Jean-Jacobs

Principal Economist

Economic News

A Cooler February for Canadian Retail Sales

April 24, 2024

Highlights

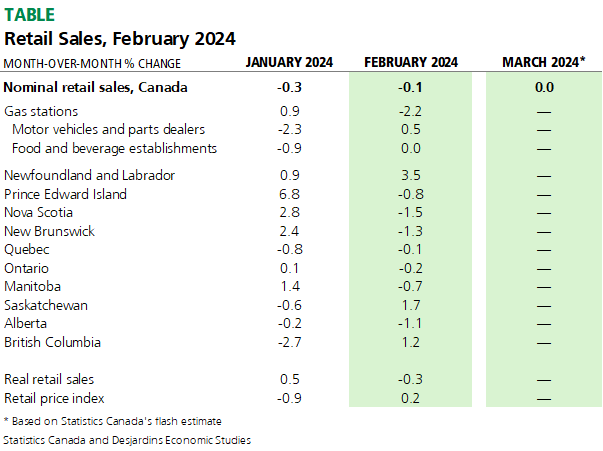

- Canadian retail sales edged down 0.1% m/m in February, a second consecutive monthly decrease after January’s 0.3% drop. This is lower than Statistics Canada’s earlier flash estimate and the consensus of economic forecasters, which pointed to an increase of 0.1%. The table below summarizes key data points.

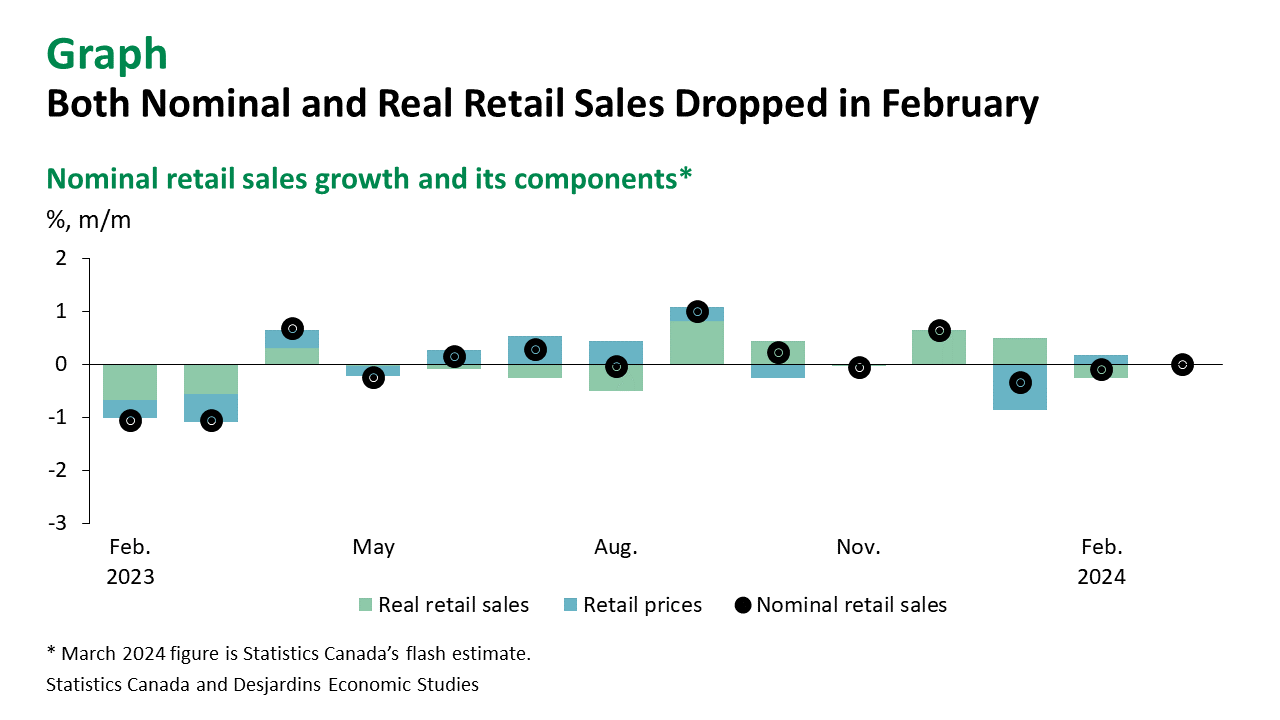

- The drop in real retail sales (-0.3%) was the most pronounced decline since last August. Higher prices (+0.2%) did not offset this drag from volumes on retail sales (graph).

- The sharp decrease in sales at gasoline stations and fuel vendors (-2.2%) was the main contributor to February’s drop in sales. If we exclude gas stations, retail sales increased 0.1% on a nominal basis. While gas prices were up, sales volumes fell.

- After contracting 2.4% in January, sales at motor vehicle and parts dealers edged up 0.5% in February. This is largely explained by other motor vehicle dealers (which include recreational vehicles, motorcycles, trailers, and watercraft). Sales of auto parts declined (-1.7%), while those at both new and used car dealers inched up 0.3%.

- Core retail sales—which exclude gasoline and auto sales—were unchanged. Higher sales of general merchandise and health and personal care products were offset by lower receipts for durables and discretionary products such as furniture, home furnishings, electronics and appliances (-1.5%), as well as clothing and accessories (-1.0%).

- Retail sales were down in seven provinces, led by Alberta (-1.1%). Ontario and Quebec experienced drops, while BC sales increased.

- Statistics Canada’s flash estimate for March nominal retail sales points to a flat print. This suggests modest growth in volumes given the 0.3% decrease m/m in seasonally adjusted goods CPI.

Implications

The February release came in cooler than anticipated. While some elements were to be expected, such as subdued demand for non-essentials and things like furniture and appliances, others were somewhat surprising. The sharp drop in gasoline sales was unexpected, although there is considerable monthly volatility in this category. As for motor vehicle sales, it looks like automobile dealerships maintained a fairly slow pace of sales, while other recreational vehicles led the upside move.

One thing is clear: given the record-high population growth in Q1, this morning’s retail print—including the decline in volumes—suggests per-person spending was even weaker than implied by the headline figure. We’ll be watching the March data closely. If the flash estimate proves correct, nominal retail sales likely stalled in Q1 (+0.1% q/q annualized) but declined by 3% on a per capita basis (q/q annualized, population ages 15 and over).

Still, January and February retail showed pockets of resilience. And with other data coming in hot in the last few weeks, our tracking suggests real annualized GDP growth in the range of 2.5% to 3% annualized in the first quarter of 2024. That’s in line with the Bank of Canada’s latest forecast of 2.8%.

Combined with inflation data pointing to further normalization in consumer price growth in March, two monthly declines in retail sales to begin 2024 suggest the Canadian economy is continuing to weaken in response to higher interest rates. Consequently, we remain of the view that the Bank of Canada is set to reduce its policy rate in June.